About us

GreenGo is a digital platform for partners who insure vehicles, cargo, and other risks when crossing borders.

Mission GreenGo

Our mission is to expand the boundaries of international insurance. Our goal is to create a convenient and profitable insurance ecosystem for all market participants. GreenGo brings together insurance market participants to provide them with a single digital tool for work.

We believe that everyone should have the opportunity to earn money honestly, transparently, and without unnecessary barriers. That is why GreenGo is not just a platform, but a full-fledged service that automates calculations, payments, and registration, reducing the time from client to finished policy to just minutes.

We believe that everyone should have the opportunity to earn money honestly, transparently, and without unnecessary barriers. That is why GreenGo is not just a platform, but a full-fledged service that automates calculations, payments, and registration, reducing the time from client to finished policy to just minutes.

We work with leading insurance companies in Russia, Kazakhstan, and Kyrgyzstan to provide users with the best conditions and maximum benefits. Our team focuses on developing a service that supports partners at every stage: from connection to scaling their own network.

We strive to make insurance simple and earnings clear and accessible.

We work with leading insurance companies in Russia, Kazakhstan, and Kyrgyzstan to provide users with the best conditions and maximum benefits. Our team focuses on developing a service that supports partners at every stage: from connection to scaling their own network.

We strive to make insurance simple and earnings clear and accessible.

How to start earning with GreenGo?

3 simple steps to earning.

Step 1

Register on our platform

Complete registration. Provide your details in your personal account to withdraw remuneration in your profile.

Step 2

Select a product and start selling

We have gathered offers from leading insurance companies. All you have to do is offer them to clients.

Step 3

Receive your income within one day

After fulfilling the transaction conditions, you will be able to withdraw money within one day.

News and useful materials

Driver assistance

KazAvtoZhol payment is now available on the GreenGo platform

GreenGo continues to expand the range of services for insurance partners. The platform now offers KazAvtoZhol payment, allowing agents to help their clients pay for travel on toll roads of the Republic of Kazakhstan in a timely manner.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties when paying for travel: they cannot use familiar Kazakh payment instruments, have problems topping up their account, or paying off debts.

These issues can now be resolved through an insurance agent working on the GreenGo platform.

The service allows you to take care of payment in advance and make traveling in Kazakhstan more comfortable.

Important: paying for travel on toll roads in Kazakhstan helps avoid debt and ensures uninterrupted use of toll road sections.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties when paying for travel: they cannot use familiar Kazakh payment instruments, have problems topping up their account, or paying off debts.

These issues can now be resolved through an insurance agent working on the GreenGo platform.

The service allows you to take care of payment in advance and make traveling in Kazakhstan more comfortable.

Important: paying for travel on toll roads in Kazakhstan helps avoid debt and ensures uninterrupted use of toll road sections.

What is KazAvtoZhol

JSC "NC "KazAvtoZhol" is the national road operator of the Republic of Kazakhstan. The company is responsible for the development, maintenance, and operation of the republican road network, as well as organizing the toll collection system on toll roads.

Today, Kazakhstan has a developed network of toll road sections. Payment is made through an electronic system, and users can monitor their account balance, pay debts, and use the KazToll personal account.

Why foreign drivers sometimes find it difficult to pay for travel

For citizens of Kazakhstan, the payment process usually does not cause difficulties. Bank cards, mobile applications, the KazToll personal account, and other familiar payment methods are available.

For foreign drivers, the situation is often different.

The most common difficulties:

That is why the ability to contact an insurance agent and resolve the payment issue in advance is especially convenient for non-residents.

For foreign drivers, the situation is often different.

The most common difficulties:

- lack of a Kazakh bank card;

- inability to quickly top up the account;

- difficulties with paying off debts;

- lack of familiarity with the KazAvtoZhol system.

That is why the ability to contact an insurance agent and resolve the payment issue in advance is especially convenient for non-residents.

Which toll roads in Kazakhstan are most commonly used by non-residents

Thousands of foreign drivers use Kazakhstan's toll roads every day. This is especially true for international carriers and travelers traveling between Central Asia, Russia, and China.

For GreenGo clients, routes regularly used by citizens of Kyrgyzstan, Uzbekistan, Russia, and China are of particular interest.

For example, drivers from Kyrgyzstan often use highways through Taraz and Shymkent when traveling to the central regions of Kazakhstan.

For citizens of Uzbekistan, the most popular route is Shymkent — Uzbekistan border, as well as the Shymkent — Taraz direction.

Companies engaged in transportation between China, Kazakhstan, and Russia regularly use toll sections of republican roads, allowing them to reduce cargo delivery times.

| Toll section | Who uses it most often | Purpose |

|---|---|---|

| Astana — Shchuchinsk | Tourists and carriers | Connects the capital with the Burabay resort area |

| Astana — Temirtau | International carriers | One of the main routes in central Kazakhstan |

| Almaty — Konayev | Tourists and residents of border regions | Trips to the Kapshagay reservoir and transit routes |

| Shymkent — Uzbekistan border | Citizens of Uzbekistan and international carriers | International route towards Tashkent |

| Shymkent — Taraz | Carriers from Kyrgyzstan and Uzbekistan | One of the most important transport corridors in southern Kazakhstan |

What advantages do insurance partners get

The launch of the new service allows agents to expand their service offering and provide clients with comprehensive trip support.

Key advantages:

Key advantages:

- additional service for existing clients;

- assistance to foreign citizens;

- solving the KazAvtoZhol payment issue;

- registration through the familiar GreenGo platform;

- increasing the value of the agent's services;

- ability to support the client not only during insurance registration but also during the trip.

When the service is especially in demand

KazAvtoZhol payment is especially relevant for:

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary organizational matters during the trip.

- international freight transportation;

- tourist trips;

- transit through Kazakhstan;

- trips between Kazakhstan, Kyrgyzstan, Uzbekistan, Russia, and China;

- regular commercial routes.

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary organizational matters during the trip.

Summary

The launch of the KazAvtoZhol payment service is another step in the development of the GreenGo ecosystem for insurance partners.

Agents can now help their clients not only with issuing insurance products but also with solving practical issues that arise during trips in Kazakhstan. This is especially relevant for foreign citizens from Kyrgyzstan, Uzbekistan, Russia, China, and other countries who may find it difficult to use local payment services.

By expanding the list of available services, GreenGo helps partners offer comprehensive service, save clients' time, and make traveling in Kazakhstan even more convenient.

Agents can now help their clients not only with issuing insurance products but also with solving practical issues that arise during trips in Kazakhstan. This is especially relevant for foreign citizens from Kyrgyzstan, Uzbekistan, Russia, China, and other countries who may find it difficult to use local payment services.

By expanding the list of available services, GreenGo helps partners offer comprehensive service, save clients' time, and make traveling in Kazakhstan even more convenient.

28 July 2026, 21:11

1495

Driver assistance

RF services

Pay for toll roads in Russia on the GreenGo platform

GreenGo continues to expand the range of services for insurance partners. The platform now offers payment for toll roads in Russia, allowing agents to help their clients pay for travel on toll highways of the Russian Federation in advance.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties paying for Russian services: they do not have a Russian bank card, familiar payment methods do not work, or there is no way to quickly top up their balance. These issues can now be resolved through an insurance agent working on the GreenGo platform.

The new service makes traveling in Russia even more comfortable and relieves clients of unnecessary organizational issues.

Important: payment for toll roads does not replace mandatory travel documents, but allows you to prepare for the route in advance and avoid inconvenience when passing through toll sections of Russian highways.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties paying for Russian services: they do not have a Russian bank card, familiar payment methods do not work, or there is no way to quickly top up their balance. These issues can now be resolved through an insurance agent working on the GreenGo platform.

The new service makes traveling in Russia even more comfortable and relieves clients of unnecessary organizational issues.

Important: payment for toll roads does not replace mandatory travel documents, but allows you to prepare for the route in advance and avoid inconvenience when passing through toll sections of Russian highways.

Why foreign drivers sometimes find it difficult to pay for toll roads in Russia

In recent years, the network of toll roads in Russia has expanded significantly. Modern highways allow you to significantly reduce travel time, make the trip more comfortable, and avoid congested road sections.

For Russian citizens, payment usually does not cause difficulties: Russian bank cards, transponders, mobile applications, and other familiar payment methods are available.

For foreign drivers, the situation is often different. Due to the lack of Russian bank cards or limited access to certain payment services, paying for travel can become an additional task during the trip.

That is why the ability to pay for toll roads in advance through an insurance agent becomes a convenient solution for non-residents.

For Russian citizens, payment usually does not cause difficulties: Russian bank cards, transponders, mobile applications, and other familiar payment methods are available.

For foreign drivers, the situation is often different. Due to the lack of Russian bank cards or limited access to certain payment services, paying for travel can become an additional task during the trip.

That is why the ability to pay for toll roads in advance through an insurance agent becomes a convenient solution for non-residents.

Which toll roads in Russia are most commonly used by non-residents

Many foreign drivers regularly use Russian federal highways. This is especially true for international freight transportation, tourist trips, and transit routes.

The most popular toll roads are presented in the table below.

| Toll road | Who uses it most often | Purpose |

|---|---|---|

| M-12 "Vostok" (Moscow — Kazan, further development towards Yekaterinburg) | Carriers and travelers from Kazakhstan | One of the main routes between Kazakhstan and central Russia |

| M-11 "Neva" (Moscow — Saint Petersburg) | Tourists, carriers, international business | Fast connection between Russia's two largest cities |

| M-4 "Don" | Tourists from Kazakhstan and CIS countries | Trips to southern Russia and the Black Sea coast |

| Central Ring Road (CRR) | International carriers | Allows bypassing Moscow without entering the city |

| Western High-Speed Diameter (WHSD) | Drivers heading to Saint Petersburg and seaports | Used for international transportation through northwestern Russia |

For GreenGo clients, routes regularly used by citizens of Kazakhstan, Kyrgyzstan, Uzbekistan, and China are of particular interest.

For example, carriers from Kazakhstan often use the M-12 "Vostok" highway, as well as the Central Ring Road (CRR) when delivering goods to Moscow and other regions of Russia.

For drivers from Kyrgyzstan and Uzbekistan, the most popular routes pass through Kazakhstan with further travel along Russian federal highways towards Moscow, Saint Petersburg, and the central part of the country.

Companies engaged in international transportation between China and Russia also actively use high-speed federal highways, allowing them to reduce cargo delivery times and increase logistics efficiency.

What payment methods for toll roads exist

Today, there are several ways to pay for travel on toll roads in Russia. However, not all of them are equally convenient for foreign citizens.

| Payment method | Suitable for RF residents | Suitable for non-residents | Features |

|---|---|---|---|

| Russian bank card | ✓ | Not always | Requires a Russian bank card |

| Transponder | ✓ | Partially | Must purchase the device and top up the balance |

| Road operator online services | ✓ | Partially | Restrictions may apply when using foreign bank cards |

| Payment through GreenGo | ✓ | ✓ | The agent helps the client pay for travel even without Russian payment instruments |

What advantages do insurance partners get

The launch of the new service allows agents to significantly expand the range of services they can offer to their clients.

Key advantages:

This approach helps the agent increase the value of their services and make cooperation with the client more long-term.

Key advantages:

- additional service for existing clients;

- assistance to foreign citizens when traveling in Russia;

- solving the payment issue for Russian toll roads;

- opportunity to offer comprehensive trip support;

- work within a single GreenGo personal account;

- increasing client loyalty through additional services.

This approach helps the agent increase the value of their services and make cooperation with the client more long-term.

When the service is especially in demand

Payment for toll roads may be needed in various situations.

The service is most often used for:

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary stops and organizational difficulties on the road.

The service is most often used for:

- tourist trips;

- international freight transportation;

- transit through Russia;

- business trips;

- regular routes between Russia, Kazakhstan, Kyrgyzstan, Uzbekistan, and China;

- vehicle and commercial cargo delivery.

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary stops and organizational difficulties on the road.

Summary

The launch of the toll road payment service is another step in the development of the GreenGo ecosystem for insurance partners.

Agents can now help their clients not only with insurance but also with solving practical issues that arise during trips in Russia. This is especially relevant for foreign citizens from Kazakhstan, Kyrgyzstan, Uzbekistan, China, and other countries who may find it difficult to use Russian payment services.

By expanding the list of available services, GreenGo helps partners offer clients comprehensive service, save their time, and make trips in Russia even more comfortable.

Agents can now help their clients not only with insurance but also with solving practical issues that arise during trips in Russia. This is especially relevant for foreign citizens from Kazakhstan, Kyrgyzstan, Uzbekistan, China, and other countries who may find it difficult to use Russian payment services.

By expanding the list of available services, GreenGo helps partners offer clients comprehensive service, save their time, and make trips in Russia even more comfortable.

21 July 2026, 14:37

3687

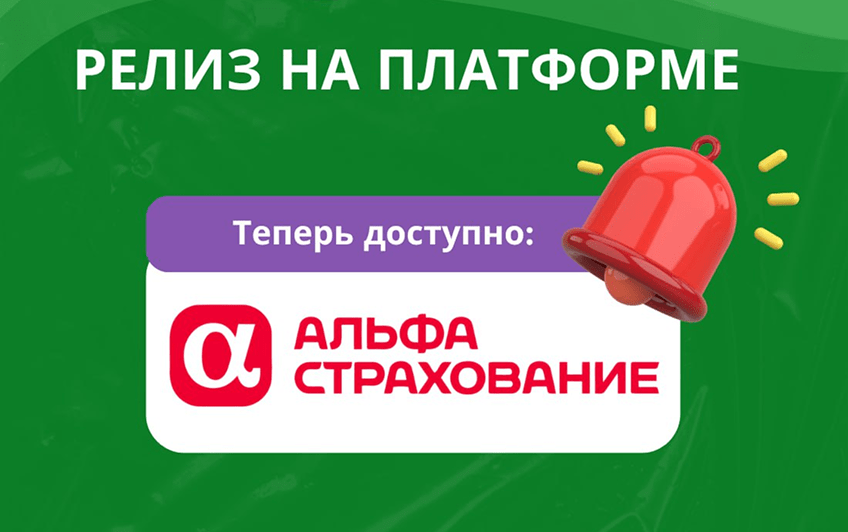

Auto insurance

OSAGO Uzbekistan for non-residents is now available on the GreenGo platform

GreenGo continues to expand opportunities for insurance partners. The platform now offers OSAGO Uzbekistan for non-residents — a new product that allows agents to quickly issue compulsory auto insurance for clients traveling to the Republic of Uzbekistan in vehicles with foreign registration.

The launch of this new direction makes the work of insurance partners even more convenient: the policy can be issued in the familiar GreenGo interface, without searching for separate insurance companies and additional services.

Previously, an agent had to independently find a suitable solution for the client, but now OSAGO Uzbekistan registration is available within a single platform.

Important

OSAGO is a compulsory type of civil liability insurance for vehicle owners. Before traveling to Uzbekistan, it is recommended to ensure in advance that the vehicle has insurance protection in accordance with legal requirements.

What is OSAGO Uzbekistan

OSAGO is compulsory civil liability insurance for vehicle owners.

If a driver is found at fault for a traffic accident, the insurance company compensates for damage caused to other road users, within the limits of the contract terms.

However, the policy does not cover repairs to the policyholder's own vehicle. For that, voluntary insurance — CASCO — exists.

In essence, the system is similar to the compulsory auto insurance in force in Russia, Kazakhstan, and other CIS countries, but registration is carried out in accordance with the legislation of the Republic of Uzbekistan.

Who will need OSAGO Uzbekistan

The new product is primarily aimed at foreign citizens who plan to use a vehicle on the territory of Uzbekistan.

Policy registration is most often required by:

- tourists;

- owners of vehicles with foreign license plates;

- entrepreneurs;

- carriers;

- company employees traveling on business trips;

- people transiting through Uzbekistan.

For insurance agents, having such a product allows them to fully address the client's request without sending them to look for insurance on their own.

Why it's better to take out a policy in advance

Many drivers start looking for insurance only after crossing the border.

In practice, this can lead to additional time costs: you need to find an insurance company, understand the registration terms, and prepare documents.

When taking out insurance in advance, the client receives a ready-made policy before the trip, and the agent can verify the accuracy of all data in advance.

This is especially convenient during peak tourist seasons or for business trips when time is of the essence.

What documents will be needed

| Document | Purpose |

|---|---|

| Passport | Policyholder identification |

| Vehicle documents | Verification of vehicle characteristics |

| License plate number | Policy registration |

| Contact details | Receiving insurance documents |

The exact list may vary depending on the terms of the specific insurance product.

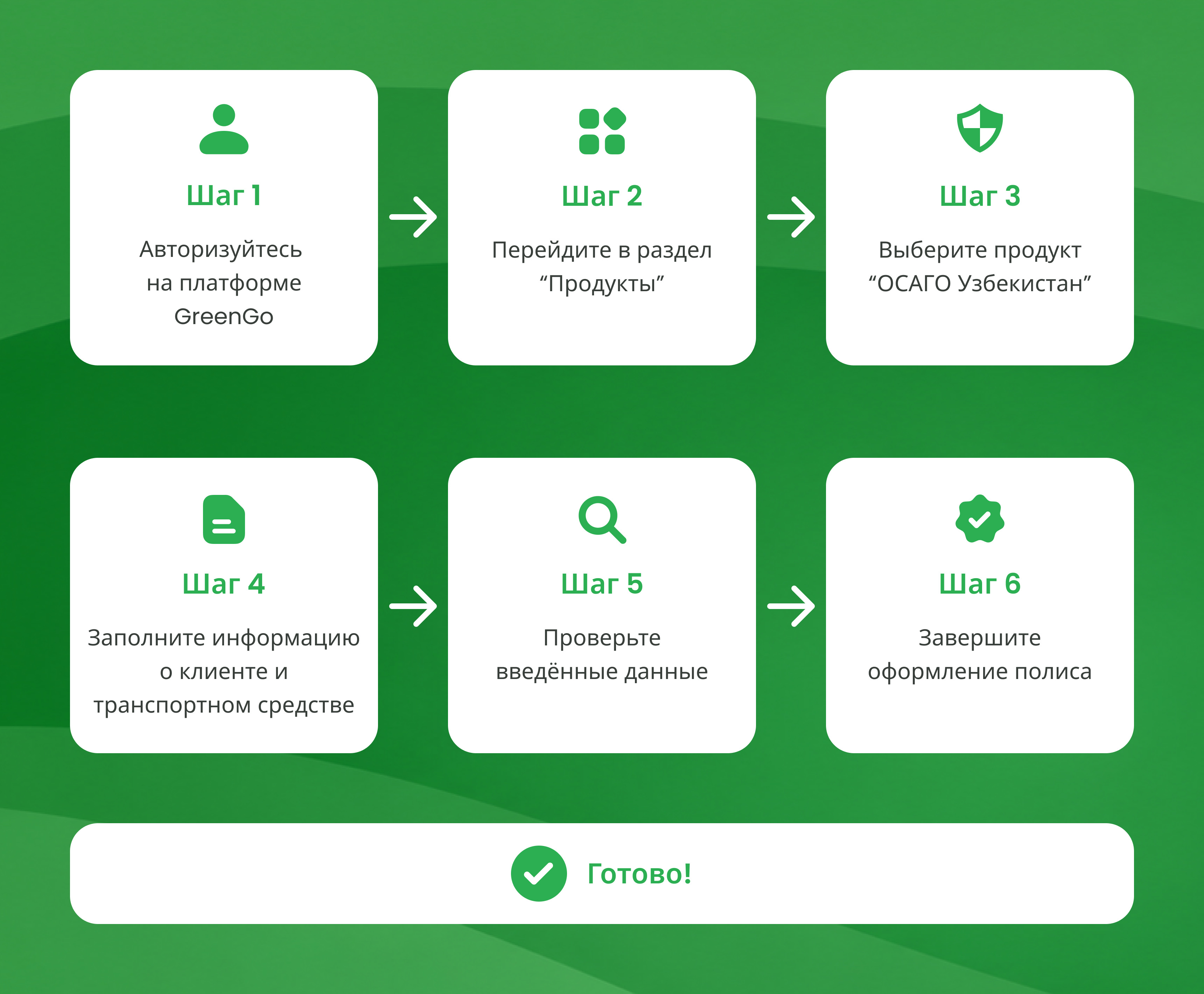

How to apply for OSAGO Uzbekistan through GreenGo

The registration process is as simple as possible.

Step 1. Log in to the GreenGo platform.

Step 2. Go to the "Products" section.

Step 3. Select the "OSAGO Uzbekistan" product.

Step 4. Fill in the information about the client and the vehicle.

Step 5. Check the entered data.

Step 6. Complete the policy registration.

After registration, the insurance document becomes available to be sent to the client.

What advantages do insurance partners get

The launch of the new product allows agents to expand their capabilities and increase the number of contracts issued.

Key advantages:

- ✅ fully online registration;

- ✅ work within a single GreenGo personal account;

- ✅ less time spent searching for insurance solutions;

- ✅ ability to offer the client an additional insurance product;

- ✅ expansion of the product range without connecting new services.

When OSAGO Uzbekistan is especially in demand

Practice shows that the policy is most often taken out before:

- tourist trips;

- seasonal travel;

- international automobile routes;

- business trips;

- freight transportation;

- long-term stays in Uzbekistan.

For an insurance agent, this means an additional opportunity to offer the client a necessary product at the trip preparation stage.

Why GreenGo

The GreenGo platform combines insurance products for non-residents in a single workspace.

Partners do not need to work with multiple services simultaneously or manually search for suitable insurance offers. All available products are gathered in a single interface, which significantly speeds up registration and reduces the likelihood of errors.

As the platform develops, the list of insurance solutions continues to expand, allowing agents to cover more and more client requests.

Summary

The addition of OSAGO Uzbekistan to the GreenGo platform is another step towards creating a unified ecosystem of insurance products for non-residents.

Insurance partners can now issue compulsory auto insurance for trips to Uzbekistan in a familiar interface, saving time on finding solutions and offering clients a more complete service.

13 July 2026, 10:21

1457

Driver assistance

KazAvtoZhol payment is now available on the GreenGo platform

GreenGo continues to expand the range of services for insurance partners. The platform now offers KazAvtoZhol payment, allowing agents to help their clients pay for travel on toll roads of the Republic of Kazakhstan in a timely manner.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties when paying for travel: they cannot use familiar Kazakh payment instruments, have problems topping up their account, or paying off debts.

These issues can now be resolved through an insurance agent working on the GreenGo platform.

The service allows you to take care of payment in advance and make traveling in Kazakhstan more comfortable.

Important: paying for travel on toll roads in Kazakhstan helps avoid debt and ensures uninterrupted use of toll road sections.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties when paying for travel: they cannot use familiar Kazakh payment instruments, have problems topping up their account, or paying off debts.

These issues can now be resolved through an insurance agent working on the GreenGo platform.

The service allows you to take care of payment in advance and make traveling in Kazakhstan more comfortable.

Important: paying for travel on toll roads in Kazakhstan helps avoid debt and ensures uninterrupted use of toll road sections.

What is KazAvtoZhol

JSC "NC "KazAvtoZhol" is the national road operator of the Republic of Kazakhstan. The company is responsible for the development, maintenance, and operation of the republican road network, as well as organizing the toll collection system on toll roads.

Today, Kazakhstan has a developed network of toll road sections. Payment is made through an electronic system, and users can monitor their account balance, pay debts, and use the KazToll personal account.

Why foreign drivers sometimes find it difficult to pay for travel

For citizens of Kazakhstan, the payment process usually does not cause difficulties. Bank cards, mobile applications, the KazToll personal account, and other familiar payment methods are available.

For foreign drivers, the situation is often different.

The most common difficulties:

That is why the ability to contact an insurance agent and resolve the payment issue in advance is especially convenient for non-residents.

For foreign drivers, the situation is often different.

The most common difficulties:

- lack of a Kazakh bank card;

- inability to quickly top up the account;

- difficulties with paying off debts;

- lack of familiarity with the KazAvtoZhol system.

That is why the ability to contact an insurance agent and resolve the payment issue in advance is especially convenient for non-residents.

Which toll roads in Kazakhstan are most commonly used by non-residents

Thousands of foreign drivers use Kazakhstan's toll roads every day. This is especially true for international carriers and travelers traveling between Central Asia, Russia, and China.

For GreenGo clients, routes regularly used by citizens of Kyrgyzstan, Uzbekistan, Russia, and China are of particular interest.

For example, drivers from Kyrgyzstan often use highways through Taraz and Shymkent when traveling to the central regions of Kazakhstan.

For citizens of Uzbekistan, the most popular route is Shymkent — Uzbekistan border, as well as the Shymkent — Taraz direction.

Companies engaged in transportation between China, Kazakhstan, and Russia regularly use toll sections of republican roads, allowing them to reduce cargo delivery times.

| Toll section | Who uses it most often | Purpose |

|---|---|---|

| Astana — Shchuchinsk | Tourists and carriers | Connects the capital with the Burabay resort area |

| Astana — Temirtau | International carriers | One of the main routes in central Kazakhstan |

| Almaty — Konayev | Tourists and residents of border regions | Trips to the Kapshagay reservoir and transit routes |

| Shymkent — Uzbekistan border | Citizens of Uzbekistan and international carriers | International route towards Tashkent |

| Shymkent — Taraz | Carriers from Kyrgyzstan and Uzbekistan | One of the most important transport corridors in southern Kazakhstan |

What advantages do insurance partners get

The launch of the new service allows agents to expand their service offering and provide clients with comprehensive trip support.

Key advantages:

Key advantages:

- additional service for existing clients;

- assistance to foreign citizens;

- solving the KazAvtoZhol payment issue;

- registration through the familiar GreenGo platform;

- increasing the value of the agent's services;

- ability to support the client not only during insurance registration but also during the trip.

When the service is especially in demand

KazAvtoZhol payment is especially relevant for:

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary organizational matters during the trip.

- international freight transportation;

- tourist trips;

- transit through Kazakhstan;

- trips between Kazakhstan, Kyrgyzstan, Uzbekistan, Russia, and China;

- regular commercial routes.

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary organizational matters during the trip.

Summary

The launch of the KazAvtoZhol payment service is another step in the development of the GreenGo ecosystem for insurance partners.

Agents can now help their clients not only with issuing insurance products but also with solving practical issues that arise during trips in Kazakhstan. This is especially relevant for foreign citizens from Kyrgyzstan, Uzbekistan, Russia, China, and other countries who may find it difficult to use local payment services.

By expanding the list of available services, GreenGo helps partners offer comprehensive service, save clients' time, and make traveling in Kazakhstan even more convenient.

Agents can now help their clients not only with issuing insurance products but also with solving practical issues that arise during trips in Kazakhstan. This is especially relevant for foreign citizens from Kyrgyzstan, Uzbekistan, Russia, China, and other countries who may find it difficult to use local payment services.

By expanding the list of available services, GreenGo helps partners offer comprehensive service, save clients' time, and make traveling in Kazakhstan even more convenient.

28 July 2026, 21:11

1495

Driver assistance

RF services

Pay for toll roads in Russia on the GreenGo platform

GreenGo continues to expand the range of services for insurance partners. The platform now offers payment for toll roads in Russia, allowing agents to help their clients pay for travel on toll highways of the Russian Federation in advance.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties paying for Russian services: they do not have a Russian bank card, familiar payment methods do not work, or there is no way to quickly top up their balance. These issues can now be resolved through an insurance agent working on the GreenGo platform.

The new service makes traveling in Russia even more comfortable and relieves clients of unnecessary organizational issues.

Important: payment for toll roads does not replace mandatory travel documents, but allows you to prepare for the route in advance and avoid inconvenience when passing through toll sections of Russian highways.

The new service is especially relevant for foreign citizens and owners of vehicles with foreign registration. In many cases, non-residents face difficulties paying for Russian services: they do not have a Russian bank card, familiar payment methods do not work, or there is no way to quickly top up their balance. These issues can now be resolved through an insurance agent working on the GreenGo platform.

The new service makes traveling in Russia even more comfortable and relieves clients of unnecessary organizational issues.

Important: payment for toll roads does not replace mandatory travel documents, but allows you to prepare for the route in advance and avoid inconvenience when passing through toll sections of Russian highways.

Why foreign drivers sometimes find it difficult to pay for toll roads in Russia

In recent years, the network of toll roads in Russia has expanded significantly. Modern highways allow you to significantly reduce travel time, make the trip more comfortable, and avoid congested road sections.

For Russian citizens, payment usually does not cause difficulties: Russian bank cards, transponders, mobile applications, and other familiar payment methods are available.

For foreign drivers, the situation is often different. Due to the lack of Russian bank cards or limited access to certain payment services, paying for travel can become an additional task during the trip.

That is why the ability to pay for toll roads in advance through an insurance agent becomes a convenient solution for non-residents.

For Russian citizens, payment usually does not cause difficulties: Russian bank cards, transponders, mobile applications, and other familiar payment methods are available.

For foreign drivers, the situation is often different. Due to the lack of Russian bank cards or limited access to certain payment services, paying for travel can become an additional task during the trip.

That is why the ability to pay for toll roads in advance through an insurance agent becomes a convenient solution for non-residents.

Which toll roads in Russia are most commonly used by non-residents

Many foreign drivers regularly use Russian federal highways. This is especially true for international freight transportation, tourist trips, and transit routes.

The most popular toll roads are presented in the table below.

| Toll road | Who uses it most often | Purpose |

|---|---|---|

| M-12 "Vostok" (Moscow — Kazan, further development towards Yekaterinburg) | Carriers and travelers from Kazakhstan | One of the main routes between Kazakhstan and central Russia |

| M-11 "Neva" (Moscow — Saint Petersburg) | Tourists, carriers, international business | Fast connection between Russia's two largest cities |

| M-4 "Don" | Tourists from Kazakhstan and CIS countries | Trips to southern Russia and the Black Sea coast |

| Central Ring Road (CRR) | International carriers | Allows bypassing Moscow without entering the city |

| Western High-Speed Diameter (WHSD) | Drivers heading to Saint Petersburg and seaports | Used for international transportation through northwestern Russia |

For GreenGo clients, routes regularly used by citizens of Kazakhstan, Kyrgyzstan, Uzbekistan, and China are of particular interest.

For example, carriers from Kazakhstan often use the M-12 "Vostok" highway, as well as the Central Ring Road (CRR) when delivering goods to Moscow and other regions of Russia.

For drivers from Kyrgyzstan and Uzbekistan, the most popular routes pass through Kazakhstan with further travel along Russian federal highways towards Moscow, Saint Petersburg, and the central part of the country.

Companies engaged in international transportation between China and Russia also actively use high-speed federal highways, allowing them to reduce cargo delivery times and increase logistics efficiency.

What payment methods for toll roads exist

Today, there are several ways to pay for travel on toll roads in Russia. However, not all of them are equally convenient for foreign citizens.

| Payment method | Suitable for RF residents | Suitable for non-residents | Features |

|---|---|---|---|

| Russian bank card | ✓ | Not always | Requires a Russian bank card |

| Transponder | ✓ | Partially | Must purchase the device and top up the balance |

| Road operator online services | ✓ | Partially | Restrictions may apply when using foreign bank cards |

| Payment through GreenGo | ✓ | ✓ | The agent helps the client pay for travel even without Russian payment instruments |

What advantages do insurance partners get

The launch of the new service allows agents to significantly expand the range of services they can offer to their clients.

Key advantages:

This approach helps the agent increase the value of their services and make cooperation with the client more long-term.

Key advantages:

- additional service for existing clients;

- assistance to foreign citizens when traveling in Russia;

- solving the payment issue for Russian toll roads;

- opportunity to offer comprehensive trip support;

- work within a single GreenGo personal account;

- increasing client loyalty through additional services.

This approach helps the agent increase the value of their services and make cooperation with the client more long-term.

When the service is especially in demand

Payment for toll roads may be needed in various situations.

The service is most often used for:

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary stops and organizational difficulties on the road.

The service is most often used for:

- tourist trips;

- international freight transportation;

- transit through Russia;

- business trips;

- regular routes between Russia, Kazakhstan, Kyrgyzstan, Uzbekistan, and China;

- vehicle and commercial cargo delivery.

In all these cases, the ability to resolve the payment issue in advance helps avoid unnecessary stops and organizational difficulties on the road.

Summary

The launch of the toll road payment service is another step in the development of the GreenGo ecosystem for insurance partners.

Agents can now help their clients not only with insurance but also with solving practical issues that arise during trips in Russia. This is especially relevant for foreign citizens from Kazakhstan, Kyrgyzstan, Uzbekistan, China, and other countries who may find it difficult to use Russian payment services.

By expanding the list of available services, GreenGo helps partners offer clients comprehensive service, save their time, and make trips in Russia even more comfortable.

Agents can now help their clients not only with insurance but also with solving practical issues that arise during trips in Russia. This is especially relevant for foreign citizens from Kazakhstan, Kyrgyzstan, Uzbekistan, China, and other countries who may find it difficult to use Russian payment services.

By expanding the list of available services, GreenGo helps partners offer clients comprehensive service, save their time, and make trips in Russia even more comfortable.

21 July 2026, 14:37

3687

Auto insurance

OSAGO Uzbekistan for non-residents is now available on the GreenGo platform

GreenGo continues to expand opportunities for insurance partners. The platform now offers OSAGO Uzbekistan for non-residents — a new product that allows agents to quickly issue compulsory auto insurance for clients traveling to the Republic of Uzbekistan in vehicles with foreign registration.

The launch of this new direction makes the work of insurance partners even more convenient: the policy can be issued in the familiar GreenGo interface, without searching for separate insurance companies and additional services.

Previously, an agent had to independently find a suitable solution for the client, but now OSAGO Uzbekistan registration is available within a single platform.

Important

OSAGO is a compulsory type of civil liability insurance for vehicle owners. Before traveling to Uzbekistan, it is recommended to ensure in advance that the vehicle has insurance protection in accordance with legal requirements.

What is OSAGO Uzbekistan

OSAGO is compulsory civil liability insurance for vehicle owners.

If a driver is found at fault for a traffic accident, the insurance company compensates for damage caused to other road users, within the limits of the contract terms.

However, the policy does not cover repairs to the policyholder's own vehicle. For that, voluntary insurance — CASCO — exists.

In essence, the system is similar to the compulsory auto insurance in force in Russia, Kazakhstan, and other CIS countries, but registration is carried out in accordance with the legislation of the Republic of Uzbekistan.

Who will need OSAGO Uzbekistan

The new product is primarily aimed at foreign citizens who plan to use a vehicle on the territory of Uzbekistan.

Policy registration is most often required by:

- tourists;

- owners of vehicles with foreign license plates;

- entrepreneurs;

- carriers;

- company employees traveling on business trips;

- people transiting through Uzbekistan.

For insurance agents, having such a product allows them to fully address the client's request without sending them to look for insurance on their own.

Why it's better to take out a policy in advance

Many drivers start looking for insurance only after crossing the border.

In practice, this can lead to additional time costs: you need to find an insurance company, understand the registration terms, and prepare documents.

When taking out insurance in advance, the client receives a ready-made policy before the trip, and the agent can verify the accuracy of all data in advance.

This is especially convenient during peak tourist seasons or for business trips when time is of the essence.

What documents will be needed

| Document | Purpose |

|---|---|

| Passport | Policyholder identification |

| Vehicle documents | Verification of vehicle characteristics |

| License plate number | Policy registration |

| Contact details | Receiving insurance documents |

The exact list may vary depending on the terms of the specific insurance product.

How to apply for OSAGO Uzbekistan through GreenGo

The registration process is as simple as possible.

Step 1. Log in to the GreenGo platform.

Step 2. Go to the "Products" section.

Step 3. Select the "OSAGO Uzbekistan" product.

Step 4. Fill in the information about the client and the vehicle.

Step 5. Check the entered data.

Step 6. Complete the policy registration.

After registration, the insurance document becomes available to be sent to the client.

What advantages do insurance partners get

The launch of the new product allows agents to expand their capabilities and increase the number of contracts issued.

Key advantages:

- ✅ fully online registration;

- ✅ work within a single GreenGo personal account;

- ✅ less time spent searching for insurance solutions;

- ✅ ability to offer the client an additional insurance product;

- ✅ expansion of the product range without connecting new services.

When OSAGO Uzbekistan is especially in demand

Practice shows that the policy is most often taken out before:

- tourist trips;

- seasonal travel;

- international automobile routes;

- business trips;

- freight transportation;

- long-term stays in Uzbekistan.

For an insurance agent, this means an additional opportunity to offer the client a necessary product at the trip preparation stage.

Why GreenGo

The GreenGo platform combines insurance products for non-residents in a single workspace.

Partners do not need to work with multiple services simultaneously or manually search for suitable insurance offers. All available products are gathered in a single interface, which significantly speeds up registration and reduces the likelihood of errors.

As the platform develops, the list of insurance solutions continues to expand, allowing agents to cover more and more client requests.

Summary

The addition of OSAGO Uzbekistan to the GreenGo platform is another step towards creating a unified ecosystem of insurance products for non-residents.

Insurance partners can now issue compulsory auto insurance for trips to Uzbekistan in a familiar interface, saving time on finding solutions and offering clients a more complete service.

13 July 2026, 10:21

1457

Health insurance

Medical insurance "Welcome as a Guest!": how to choose the right program

When traveling to another country, it is important to take care not only of the route and documents, but also of medical protection. Even a routine doctor's visit or emergency care can lead to significant expenses if you don't take out an insurance policy in advance.

That is why a new product has appeared on the GreenGo platform — "Welcome as a Guest!". It allows you to quickly take out medical insurance for your stay in Russia, choose a program with the necessary level of coverage, and select a policy validity period depending on the length of your trip.

The product includes three insurance programs, including a special tariff for children, and you can take out a policy completely online in just a few minutes.

That is why a new product has appeared on the GreenGo platform — "Welcome as a Guest!". It allows you to quickly take out medical insurance for your stay in Russia, choose a program with the necessary level of coverage, and select a policy validity period depending on the length of your trip.

The product includes three insurance programs, including a special tariff for children, and you can take out a policy completely online in just a few minutes.

What is the "Welcome as a Guest!" program

"Welcome as a Guest!" is a voluntary health insurance program designed for foreign citizens coming to Russia for various periods.

The insurance policy helps to receive the necessary medical care in the event of an insured event and reduces possible financial expenses during your stay in the country.

Several program options are available on the GreenGo platform, allowing you to choose the optimal solution for almost any category of clients.

Important: all programs are issued completely online through the GreenGo platform without the need to visit an office.

The insurance policy helps to receive the necessary medical care in the event of an insured event and reduces possible financial expenses during your stay in the country.

Several program options are available on the GreenGo platform, allowing you to choose the optimal solution for almost any category of clients.

Important: all programs are issued completely online through the GreenGo platform without the need to visit an office.

Who is the program suitable for

The insurance product is designed for a wide range of clients.

It is primarily suitable for:

- foreign citizens planning a trip to Russia;

- tourists;

- people visiting relatives or friends;

- those planning a long-term stay in the country;

- families traveling with children.

Thanks to several insurance options, an agent can choose a program for almost any situation.

What programs are available

Three insurance options are currently available.

Option 1.2

A basic program for adults that includes the most in-demand medical services.

The insurance coverage includes:

This option is suitable for most clients who need reliable medical insurance during their stay in Russia.

Option 1.2

A basic program for adults that includes the most in-demand medical services.

The insurance coverage includes:

- outpatient care;

- home visits by a doctor;

- telemedicine consultations;

- immunoprophylaxis;

- emergency medical care;

- emergency hospitalization.

This option is suitable for most clients who need reliable medical insurance during their stay in Russia.

Option 1.3

An extended medical insurance program.

In addition to the basic coverage, it provides additional services, including repatriation and a broader scope of insurance protection.

This option is recommended for clients who:

An extended medical insurance program.

In addition to the basic coverage, it provides additional services, including repatriation and a broader scope of insurance protection.

This option is recommended for clients who:

- plan a long-term stay;

- want the widest possible medical coverage;

- prefer additional insurance guarantees.

Option 1.9

A special program for children. The program includes:

A special program for children. The program includes:

- outpatient treatment;

- home visits by a doctor;

- telemedicine;

- immunoprophylaxis;

- emergency care;

- emergency hospitalization.

Comparison of programs

| Program | Who it is for | Features |

|---|---|---|

| Option 1.2 | Adults | Basic medical protection |

| Option 1.3 | Adults | Extended coverage, additional services and repatriation |

| Option 1.9 | Children | Special medical insurance program for children |

For what period can the policy be issued

The GreenGo platform offers four options for the insurance policy validity period.

The following insurance periods are available:

This selection allows you to choose insurance for almost any travel purpose.

The following insurance periods are available:

- 1 month — for short-term trips;

- 3 months — optimal for a longer visit;

- 6 months — suitable for extended stays;

- 12 months — a solution for those planning a long-term stay in Russia.

This selection allows you to choose insurance for almost any travel purpose.

What is included in the insurance coverage

Depending on the chosen program, the client may have access to the following medical services:

The specific list of services depends on the chosen insurance option.

- outpatient medical care;

- doctor consultations;

- home care;

- telemedicine consultations;

- immunoprophylaxis;

- emergency medical services;

- emergency and urgent hospitalization;

- repatriation (for the extended program).

The specific list of services depends on the chosen insurance option.

How to choose the right program

When choosing an insurance policy, it is worth considering the purpose of the trip, the length of stay, and the client's individual needs.

In most cases, you can focus on the following recommendations:

This approach helps to quickly select the optimal insurance product.

In most cases, you can focus on the following recommendations:

| If the client... | Recommended program |

|---|---|

| Is planning a short trip | Option 1.2 |

| Wants maximum insurance protection | Option 1.3 |

| Is traveling with a child | Option 1.9 |

Why insurance agents find it convenient to work through GreenGo

The GreenGo platform significantly reduces the time required to issue insurance products.

Key advantages:

Thanks to this, an agent can issue a policy in just a few minutes.

Key advantages:

- fully online registration;

- three insurance program options;

- choice of policy validity period;

- special program for children;

- simple and intuitive interface;

- quick document processing;

- ability to choose the optimal solution for each client.

Thanks to this, an agent can issue a policy in just a few minutes.

Conclusion

The "Welcome as a Guest!" program allows you to choose medical insurance for various categories of clients and issue a policy completely online through the GreenGo platform.

Three insurance options, the ability to choose a period from one month to one year, as well as a separate program for children, make the product a universal solution for both short-term trips and long-term stays in Russia.

If you are already working with the GreenGo platform, the new product is available for registration in your personal account.

Three insurance options, the ability to choose a period from one month to one year, as well as a separate program for children, make the product a universal solution for both short-term trips and long-term stays in Russia.

If you are already working with the GreenGo platform, the new product is available for registration in your personal account.

03 July 2026, 14:45

2368

Auto insurance

Auto insurance in 2026 and beyond: how the market is changing and why a systematic approach is becoming decisive

Auto insurance in 2026 and beyond: how the market is changing and why a systematic approach is becoming decisive

Auto insurance is entering a new stage of development.

Changes in regulation, rising repair and parts costs, and the digitalization of government services are shaping a more demanding and transparent environment. In 2026, the insurance market is finally moving away from a formal approach to policies and is increasingly focusing on real protection and convenience for clients.

For insurance market professionals, this is not just another change — it is a growth point. Those who adapt in advance gain an advantage in stability and quality of work.

Changes in regulation, rising repair and parts costs, and the digitalization of government services are shaping a more demanding and transparent environment. In 2026, the insurance market is finally moving away from a formal approach to policies and is increasingly focusing on real protection and convenience for clients.

For insurance market professionals, this is not just another change — it is a growth point. Those who adapt in advance gain an advantage in stability and quality of work.

Strengthening control and digital policy verification

One of the key areas of development is the automatic monitoring of the presence and validity period of OSAGO policies. Regulators are increasingly implementing digital monitoring mechanisms to reduce the number of uninsured vehicles on the roads.

In Russia, for example, the implementation of OSAGO verification using road cameras has been discussed and gradually prepared for several years.

At the same time, the digital ecosystem "Gosuslugi Auto" is developing, making data on vehicles and policies more accessible to drivers.

In Russia, for example, the implementation of OSAGO verification using road cameras has been discussed and gradually prepared for several years.

At the same time, the digital ecosystem "Gosuslugi Auto" is developing, making data on vehicles and policies more accessible to drivers.

What this means for the market

For the market, this means one thing: the absence of a policy or a missed expiration date is becoming increasingly noticeable, and clients' attention to auto insurance is inevitably growing.

Revision of tariffs and limits: a response to rising real costs

Alongside the strengthening of control, there is a revision of tariff corridors and liability limits. In recent years, the cost of car repairs, parts, towing, and medical services has increased significantly.

As a result, previous coverage limits are increasingly insufficient for real situations on the road. That is why regulators in different countries are adjusting the parameters of compulsory auto insurance, striving to bring insurance coverage closer to actual expenses.

For clients, this changes the perception of the product: the policy is increasingly seen not as a formal requirement but as a financial protection tool, the quality of which determines peace of mind in the event of an accident.

As a result, previous coverage limits are increasingly insufficient for real situations on the road. That is why regulators in different countries are adjusting the parameters of compulsory auto insurance, striving to bring insurance coverage closer to actual expenses.

For clients, this changes the perception of the product: the policy is increasingly seen not as a formal requirement but as a financial protection tool, the quality of which determines peace of mind in the event of an accident.

New client behavior in 2026+

Modern car owners are becoming more attentive and informed. More and more clients:

That is why in 2026, the role of systematic support and competent navigation through insurance products is increasing.

- check the policy validity period in advance;

- want to see several calculation options;

- expect fast online service;

- value transparent terms without "fine print".

That is why in 2026, the role of systematic support and competent navigation through insurance products is increasing.

Why the partner's role is becoming key

In the context of automatic control and digitalization, the partner ceases to be just a document processor. Their value shifts towards:

- timely renewal reminders;

- correct explanations of terms;

- assistance in choosing the right option;

- client support throughout the entire policy period.

How GreenGo helps work in the new reality

The GreenGo platform combines in one space the tools that allow you to work calmly and consistently:

GreenGo allows you to quickly calculate auto insurance online, work with trusted insurance companies, see the history of all registrations, and track renewal deadlines in advance. The renewal tool helps not to lose "warm" clients, while the convenient balance and digital processes allow you to complete tasks without unnecessary delays.

As a result, the partner works not in constant reaction mode, but in control and planning mode.

GreenGo allows you to quickly calculate auto insurance online, work with trusted insurance companies, see the history of all registrations, and track renewal deadlines in advance. The renewal tool helps not to lose "warm" clients, while the convenient balance and digital processes allow you to complete tasks without unnecessary delays.

As a result, the partner works not in constant reaction mode, but in control and planning mode.

Why starting to work through GreenGo is strategically correct

In an environment where the market is becoming more transparent and demanding, those who win are those who:

- minimize manual routine;

- build long-term relationships with clients;

- use digital tools instead of chaotic processes;

- work for sustainable results, not one-off deals.

Conclusion

Auto insurance in 2026 is a market where control is strengthening, terms are being revised, and the value of a systematic approach is growing. Clients expect convenience, transparency, and timely support, while partners expect tools that help them work without being overwhelmed.

GreenGo helps you fit into these changes calmly and professionally, turning market demands into opportunities for growth.

👉 Start working with auto insurance through GreenGo and build sustainable results in 2026 and beyond!

GreenGo — expanding the boundaries of insurance 💚

GreenGo helps you fit into these changes calmly and professionally, turning market demands into opportunities for growth.

👉 Start working with auto insurance through GreenGo and build sustainable results in 2026 and beyond!

GreenGo — expanding the boundaries of insurance 💚

04 March 2026, 10:15

1547

Auto insurance

Fake policies: how fraud undermines the market and why the official path is critically important

Fake policies: how fraud undermines the market and why the official path is critically important

Online insurance registration has made the market more convenient and faster. But along with this, another phenomenon has emerged — a rise in fake offers, counterfeit documents, and gray schemes that are almost indistinguishable from legal registration.

Experts and government agencies in different countries are increasingly recording cases where drivers and partners encounter invalid policies — sometimes not finding out about it until their first accident.

Experts and government agencies in different countries are increasingly recording cases where drivers and partners encounter invalid policies — sometimes not finding out about it until their first accident.

Why the topic of fake policies has become relevant right now

The digitalization of auto insurance is accelerating:

But where demand grows, fraudulent schemes also appear. Their goal is to get money for a policy that:

- online registration has become the norm,

- clients want it "fast and without unnecessary questions",

- the market is expanding due to new drivers and regions.

But where demand grows, fraudulent schemes also appear. Their goal is to get money for a policy that:

- is not registered in the official database,

- is issued in someone else's name,

- or has no legal force at all.

Russia: fake OSAGO and counterfeit websites

In Russia, the Ministry of Internal Affairs and investigative authorities have officially confirmed cases where fraudsters sold invalid OSAGO policies through fake websites that visually copied the pages of insurance companies.

According to RBC, such schemes lead to the driver finding out about the problem only after an accident, when the insurance company refuses to pay because the policy is not in the registry.

Experts also note that fake policies can look absolutely correct — with seals, QR codes, and PDF files, but not be registered with the RSA.

According to RBC, such schemes lead to the driver finding out about the problem only after an accident, when the insurance company refuses to pay because the policy is not in the registry.

Experts also note that fake policies can look absolutely correct — with seals, QR codes, and PDF files, but not be registered with the RSA.

📌 Conclusion: the appearance of a document is no longer a guarantee of its authenticity — only official registration matters.

Kazakhstan: counterfeit documents and "gray" registration schemes

In Kazakhstan, government agencies have officially warned about the spread of counterfeit documents that imitate official papers — with logos, seals, and signatures.

Additionally, Kazakh media have reported cases where drivers were offered "cheap OSAGO", but upon verification:

📌 Trend: the more actively the market moves online, the more important a transparent source of registration becomes.

Additionally, Kazakh media have reported cases where drivers were offered "cheap OSAGO", but upon verification:

- the policy was not found in the database,

- it was issued to another person,

- or it was not valid when an insured event occurred.

📌 Trend: the more actively the market moves online, the more important a transparent source of registration becomes.

Kyrgyzstan: market growth — growth of responsibility

In Kyrgyzstan, the auto insurance market is actively growing amid increased control and the implementation of violation recording systems.

Experts note that against the backdrop of growing demand, attempts are also appearing to:

In such cases, the risks are borne not only by the driver but also by the partner through whom the registration was processed.

Experts note that against the backdrop of growing demand, attempts are also appearing to:

- issue a policy using forged documents,

- use fictitious data,

- use insurance in staged accident schemes.

In such cases, the risks are borne not only by the driver but also by the partner through whom the registration was processed.

Uzbekistan: digitalization and new vulnerabilities

In Uzbekistan, regulators emphasize the importance of taking out insurance exclusively through official insurance companies and platforms, as the online environment has simplified not only the process but also fraud.

The market has recorded cases of:

📌 Conclusion: digitalization requires not speed, but control and transparency.

The market has recorded cases of:

- registration without transferring data to official databases,

- offers to "get it faster and cheaper" outside the system,

- the policy having no legal force upon verification.

📌 Conclusion: digitalization requires not speed, but control and transparency.

Why the official path is no longer an "option" but a necessity

All these cases share one thing:

problems arise where there is no transparency and official registration.

That is why it is fundamentally important that when working through GreenGo:

This protects:

If doubts arise during registration regarding documents or client behavior — it is better to stop and contact your curator. Sometimes refusing a questionable registration is the best way to protect your business.

problems arise where there is no transparency and official registration.

That is why it is fundamentally important that when working through GreenGo:

- policies are issued directly through insurance companies;

- data is automatically transferred to official databases (NSIS and analogues);

- the client immediately receives a PDF document and electronic policy;

- the partner retains a complete history of registrations and accruals.

This protects:

- the client — from losing money and a false sense of security;

- the partner — from reputational and legal risks;

- the market — from distrust in insurance as a whole.

If doubts arise during registration regarding documents or client behavior — it is better to stop and contact your curator. Sometimes refusing a questionable registration is the best way to protect your business.

26 February 2026, 11:30

892

Auto insurance

Renewals in GreenGo: how to retain clients and build a regular flow of registrations

The "Renewals" section on the GreenGo platform is your working tool that helps you remind clients about renewal in time, not lose deals, and build a regular flow of registrations without chaos in notes, spreadsheets, and reminders.

In short: the system itself suggests who to write to and when, and you act calmly, confidently, and professionally.

In short: the system itself suggests who to write to and when, and you act calmly, confidently, and professionally.

Why renewals are the foundation of stable results

In insurance, sustainable growth is most often built not on the constant search for new clients, but on long-term relationships with those who already trust you. Working with an existing client base allows you to build a more predictable process and reduce the burden of acquisition.

For a client, policy renewal is a familiar and understandable step. It is important for them to be reminded of the deadline in advance and offered a convenient, clear registration format without unnecessary actions.

That is why systematic work with renewals becomes an important element of a professional approach. The "Renewals" section helps to build communication in a timely manner, maintain contact with clients, and form a stable foundation for further work.

For a client, policy renewal is a familiar and understandable step. It is important for them to be reminded of the deadline in advance and offered a convenient, clear registration format without unnecessary actions.

That is why systematic work with renewals becomes an important element of a professional approach. The "Renewals" section helps to build communication in a timely manner, maintain contact with clients, and form a stable foundation for further work.

What are "Renewals" in GreenGo

This is the section where all policies are collected that:

The platform automatically groups them by date, shows key numbers, and helps quickly find the right policy through search and filters.

As a result, you:

✅ don't keep deadlines in your head

✅ don't miss renewals

✅ work from a clear list

✅ plan tasks for the week and month

✅ increase client return rates

- need to be renewed already,

- or will need renewal soon.

The platform automatically groups them by date, shows key numbers, and helps quickly find the right policy through search and filters.

As a result, you:

✅ don't keep deadlines in your head

✅ don't miss renewals

✅ work from a clear list

✅ plan tasks for the week and month

✅ increase client return rates

What will you see in the "Renewals" section

1) Renewal statistics: numbers that help with planning

The section shows key indicators that usually have to be calculated manually:

Why this is important:

when you see the numbers, you start working not "on feelings" but systematically:

- how many policies are currently up for renewal;

- potential sales amount (how much can be issued upon renewal);

- average check;

- renewal percentage (how well you retain clients).

Why this is important:

when you see the numbers, you start working not "on feelings" but systematically:

- you understand how many tasks are actually in progress,

- you can set a goal to "close X renewals per week",

- you see growth and progress.

2) Renewal calendar: who is urgent, who is upcoming, and where you can work calmly

The platform distributes policies by time categories — this is convenient because you immediately see priorities:

Why this is convenient: you no longer dig through your client base. The system itself forms a funnel for you by time — from urgent to planned.

- expired in the last 30 days

These are clients who might have already gone to others. But often they are still ready to renew — if you write quickly and correctly. - expiring in the next 30 days

The most attractive category. The client doesn't need to decide urgently yet, but they are already ready to discuss. Soft reminders work great here. - expiring in the next 90 days

This is your calm planning zone. You can build communication in advance and distribute tasks so that there are no backlogs later.

Why this is convenient: you no longer dig through your client base. The system itself forms a funnel for you by time — from urgent to planned.

3) Smart search and filters: find the right renewal in seconds

When there are many renewals, speed is important. On GreenGo you can:

Why this is needed in practice:

- filter by policy type;

- select the desired period by date;

- quickly find a specific client / registration.

Why this is needed in practice:

- you open the section → filter "in the next 30 days" → work through the list;

- or a client writes to you → you find their renewal → quickly resolve the issue.

How does this affect income?

✅ 1) You stop losing clients due to forgetfulness

Renewals close this gap: the system reminds you, and you act according to plan.

✅ 2) You work in order, not in chaos

The problem with notes and spreadsheets is that they don't update automatically.

Renewals are a live list that is always up to date.

Renewals are a live list that is always up to date.

✅ 3) Renewals provide regularity

One-time registrations always come "in waves".

Renewals form a stable flow of tasks that allows you to:

Renewals form a stable flow of tasks that allows you to:

- plan your workload;

- distribute income more evenly;

- feel confident throughout the month.

✅ 4) Clients appreciate care, not a sale

A timely message is perceived as attention and service:

"Oh, good that you reminded me."

"Thanks, I was just about to take care of it."

"Let's renew."

"Oh, good that you reminded me."

"Thanks, I was just about to take care of it."

"Let's renew."

How to work correctly with renewals

Here is a simple algorithm that helps not to get overwhelmed while keeping everything under control.

Step 1. Start your day/week with the "30 days" category

This is the most convenient range:

not too early, but already relevant.

not too early, but already relevant.

Step 2. Write briefly, calmly, and to the point

One of the best formats:

Important:

Hello! Just a reminder that your policy is expiring soon.

I can help with renewal — it will take a couple of minutes. Shall I calculate it for you?

I can help with renewal — it will take a couple of minutes. Shall I calculate it for you?

Important:

- address by name;

- don't overload with details;

- suggest an action ("calculate today?").

Step 3. Record the result

Renewals help you keep the picture: what's in progress, what's closed, what needs attention.

Step 4. Plan ahead for the week using "90 days"

This helps avoid last-minute rushes at the end of the month.

Frequently asked questions about renewals

"And if the policy has already expired — is it worth writing?"

Yes. Many people put off renewal even if the deadline has passed. If you write correctly and calmly, you can win the client back.

"Won't this seem pushy?"

If you write in advance and to the point — no. It looks like service. Especially if you offer help rather than pressure.

"How many times should I remind?"

Usually, the following is enough:

- 1 reminder 30 days before,

- 1 — 7–10 days before,

- 1 — on the expiration day (if needed).

Conclusion

The "Renewals" section in GreenGo is a tool that:

Instead of "remembering who to write to", you simply open the section and see a ready-made action plan.

- helps retain clients,

- reduces losses,

- simplifies planning,

- makes work calmer,

- and provides stability in results.

Instead of "remembering who to write to", you simply open the section and see a ready-made action plan.

✅ Go to the "Renewals" section right now and see which renewals you have in the next 30 and 90 days. This is the simplest step that quickly turns into results.

15 January 2026, 09:45

2341

Auto insurance

What to do in case of an accident: a detailed guide for drivers and clients

A traffic accident always happens unexpectedly. Even if the accident is minor, a person experiences stress, confusion, and many questions in the moment: who to call, what to document, can they leave, what documents are needed, and how to avoid mistakes that will later complicate receiving a payment.

In practice, most difficulties in settlement arise not from the accident itself, but from incorrect actions in the first minutes after it. That is why it is important to understand the procedure in advance and act calmly and consistently.

In this article, we have analyzed how to behave correctly in an accident so that the settlement process goes as smoothly as possible and without unnecessary nerves.

In practice, most difficulties in settlement arise not from the accident itself, but from incorrect actions in the first minutes after it. That is why it is important to understand the procedure in advance and act calmly and consistently.

In this article, we have analyzed how to behave correctly in an accident so that the settlement process goes as smoothly as possible and without unnecessary nerves.

The first minutes after an accident: the main thing is not to panic

The most important thing to do immediately after an incident is to pause and calm down. Panic prevents you from assessing the situation soberly and often leads to mistakes: some people leave the scene of the accident, some forget to document the damage, and some start arguing with the other party.

After stopping the car, you must turn on the hazard lights and ensure the situation is safe for all participants. If there are injuries, the priority is to call emergency services. In other cases, it is important not to move the vehicle until the incident is documented, unless required by safety rules or traffic officers.

After stopping the car, you must turn on the hazard lights and ensure the situation is safe for all participants. If there are injuries, the priority is to call emergency services. In other cases, it is important not to move the vehicle until the incident is documented, unless required by safety rules or traffic officers.

Documenting the accident — the basis for smooth settlement

Even if the damage seems minor, documenting the accident is a mandatory step. A modern smartphone fully handles this task if used correctly.

It is recommended to document the scene from different angles, take a wide shot, the position of the vehicles, road signs and markings, as well as close-up shots of the damage. This material will help the insurance company assess the situation objectively and significantly reduce the number of clarifying questions.

The more thoroughly the circumstances of the accident are documented, the easier and faster the subsequent settlement will be.

It is recommended to document the scene from different angles, take a wide shot, the position of the vehicles, road signs and markings, as well as close-up shots of the damage. This material will help the insurance company assess the situation objectively and significantly reduce the number of clarifying questions.

The more thoroughly the circumstances of the accident are documented, the easier and faster the subsequent settlement will be.

How to know if you need to call the traffic police

In some situations, it is enough to complete a European accident report, but there are cases where you cannot do without traffic police officers. This applies to accidents with injuries, disputes between participants, significant damage, or damage to third-party property.

It is important to remember that an incorrectly chosen method of documentation can lead to delays or even denial of payment. If in doubt, it is better to consult with the insurance company — specialists will advise on how to act correctly in your specific situation.

It is important to remember that an incorrectly chosen method of documentation can lead to delays or even denial of payment. If in doubt, it is better to consult with the insurance company — specialists will advise on how to act correctly in your specific situation.

Contacting the insurance company: the sooner, the better

After documenting the accident, the next step is to contact the insurance company. Contacts are always listed on the policy, as well as available on the official websites of insurance companies and on the GreenGo platform in the "Help" → "Settlement" section.

During the first call, the insurance specialist will explain the procedure, advise what documents will be required, and provide guidance on timelines. The sooner the client gets in touch, the faster and calmer the process goes.

In practice, it is early contact that allows avoiding misunderstandings and delays in settlement.